Introduction: The New York Warning

Following the legalization of adult-use cannabis, the New York market transitioned from “grey market awareness” to “compliant retail” in an incredibly short window. This process released years of pent-up demand, but it also triggered a rapid influx of capital and established brands that began reshaping the landscape overnight.

This phenomenon is not unique to New York; it is a common trajectory for newly legalized, high-population markets such as Ohio, as well as future or pending adult-use opportunities such as Pennsylvania and Florida. Ohio launched adult-use sales in August 2024, while Pennsylvania’s 2026-27 budget proposal again includes adult-use legalization and Florida’s 2024 adult-use amendment was defeated, according to official state election records. While local brands theoretically hold the “home-field advantage,” the reality is sobering: New York’s market now shows how quickly brand rankings can shift once compliant retail, local processing, and brand licensing become available. Headset’s 24-month New York brand-ranking analysis describes a market where several brands rose or fell rapidly between March 2024 and February 2026.

This is not merely a price war. It is a multi-layered market entry advantage executed by mature brands using brand licensing, pre-existing brand equity, proven SKU systems, and superior resource reserves. For local brands, this is not just product competition; it is a race against time and structure. Recognizing the competitor’s playbook and leveraging the current temporary regulatory window is the only path to survival.

For reference, New York’s Office of Cannabis Management allows an Adult-Use Processor Type 3 Branding License, which authorizes brand licensees to enter white-label agreements with duly licensed New York processors. That structure makes it easier for established brands to enter without building a full plant-touching operation from scratch.

| Rank |

Brand Name |

State of Origin / Base |

Brand Attribute & Market Positioning |

| 1 |

Jaunty |

New York (Native) |

The king of the local value market; consistent high-volume driver. |

| 2 |

Ayrloom |

New York (Upstate) |

The current market sales giant; backed by century-old local family agro-capital. |

| 3 |

Fernway |

Massachusetts |

Powerhouse regional invader; the #1 vape brand in New England. |

| 4 |

Rove |

California |

West Coast major; established deep, compliant local supply chain infrastructure within NY. |

| 5 |

MFNY |

New York (Hudson Valley) |

Absolute top-tier favorite in the premium/connoisseur segment (Live Rosin/Resin). |

| 6 |

Florist Farms |

New York (Cortland) |

Leading local organic and regenerative agriculture farm-backed brand. |

| 7 |

PAX |

California |

Legacy nationwide hardware pioneer; the original innovator of cannabis vaping ecosystems. |

| 8 |

Hashtag Honey |

New York (Long Island) |

Local artisanal, small-batch extract brand focusing on craft quality. |

| 9 |

Cannabals |

New York (Rochester) |

In-house value brand launched by a major local licensed processor (Hemp Hunter Labs). |

| 10 |

Holiday |

Massachusetts |

Out-of-state challenger featuring highly recognizable, lifestyle-oriented concept packaging. |

| 11 |

Mfused |

Washington State |

Pacific Northwest concentrate giant; aggressively expanding eastward into the Mid-Atlantic. |

| 12 |

Heavy Hitters |

California |

Legacy West Coast heavy-hitter brand known for high potency and massive vapor production. |

| 13 |

Untitled |

New York (Native) |

Rising local hype brand; focuses on high-quality oil without the premium branding markup. |

| 14 |

Jetty Extracts |

California |

Renowned California legacy brand; the gold standard for pure, solventless Live Resin. |

| 15 |

Select |

Oregon |

Managed by MSO giant Curaleaf; boasts one of the largest footprint distribution networks nationwide. |

| 16 |

STIIIZY |

California |

Top-selling proprietary pod system and lifestyle streetwear powerhouse from the West Coast. |

| 17 |

Brass Knuckles |

California |

Legendary, hard-hitting West Coast legacy 510-cartridge brand with deep street-culture roots. |

| 18 |

New York Honey (NY Honey) |

New York (Native) |

Bottom-up value market disruptor famous for its signature high-volume syringe oil fills. |

| 19 |

Sapphire Farms |

Michigan |

Prominent Midwest commercial outdoor cultivator making its play in the Eastern market. |

| 20 |

Off Hours |

New York (Native) |

Local lifestyle brand; successfully leveraged its nano-emulsified edible hype into the vape sector. |

| 21 |

Dime Industries |

California |

Premium hardware-centric brand known for heavy industrial aesthetics and custom battery pairings. |

| 22 |

ghost. |

California |

Hype-driven California brand catering to younger demographics with high-flavor disposable pens. |

| 23 |

Nanticoke |

New York (Southern Tier) |

Multi-generational family farm transitioned brand; steady grassroots presence. |

| 24 |

RYTHM |

Illinois |

Premium flagship vape brand under Green Thumb Industries (GTI), a top-tier national MSO. |

| 25 |

Bloom |

California |

Decade-long West Coast staple specializing in true-to-strain, classic terpene profiles. |

| 26 |

Turn |

California |

West Coast viral sensation; leading the market in sleek, minimalist, tech-forward disposable pods. |

| 27 |

Eureka |

California |

Established extraction brand since 2011; scaled into a multi-state operation. |

| 28 |

High Garden |

California (Northern) |

Rooted in NorCal artisanal greenhouse cultivation; promotes clean, natural vibes. |

| 29 |

Magnitude |

Colorado |

Value-tier heavy-cartridge sub-brand engineered by national MSO PharmaCann. |

| 30 |

Littles |

New York (Native) |

Emerging pocket-sized, high-potency disposable line seeing rapid dispensary adoption locally. |

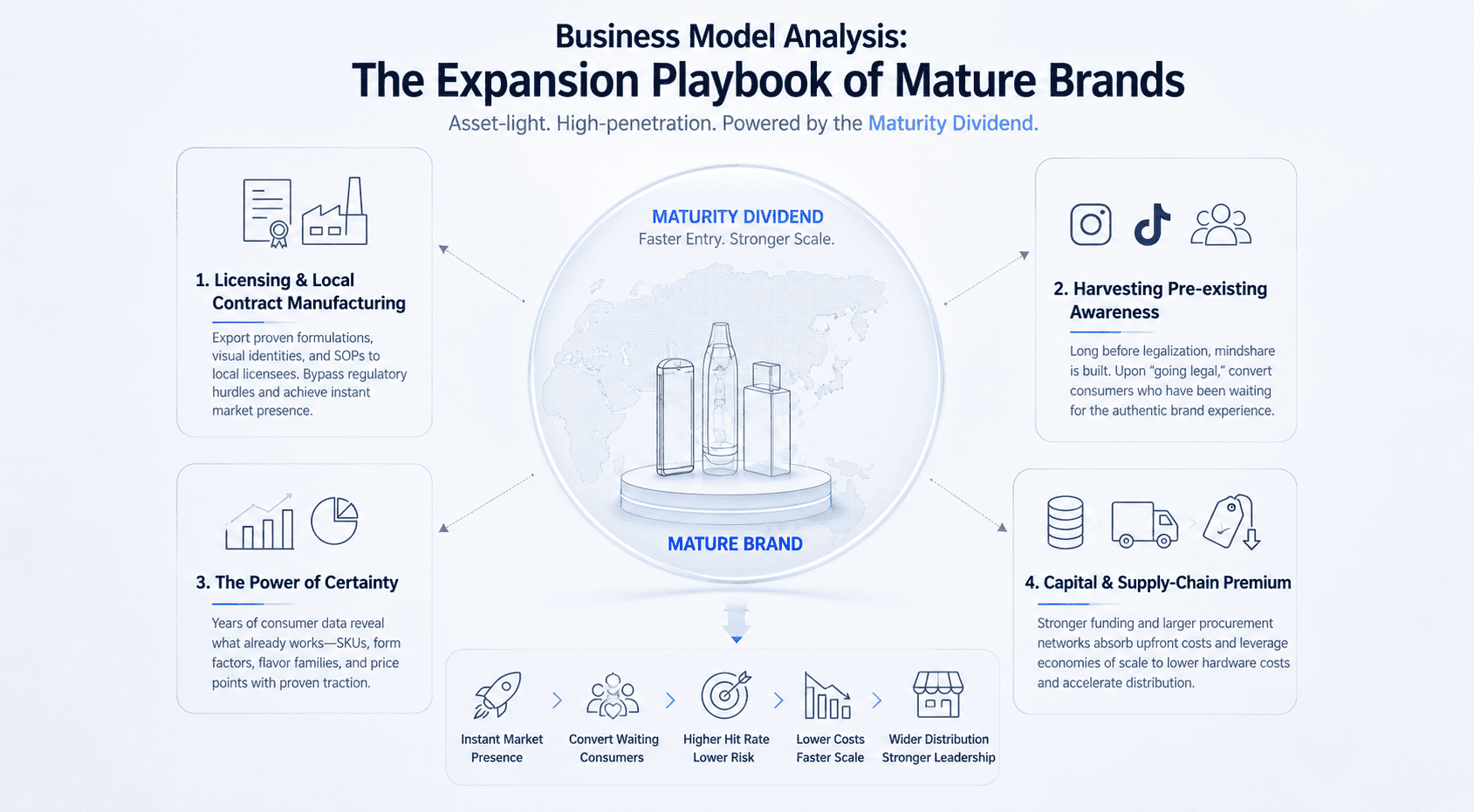

I. Business Model Analysis: The Expansion Playbook of Mature Brands

Mature brands entering new Eastern markets utilize an “asset-light, high-penetration” strategy, powered by what we call the “maturity dividend”:

-

- Licensing and local contract manufacturing: Instead of building infrastructure, they export proven formulations, visual identities, and SOPs to local licensees, bypassing regulatory hurdles to achieve instant market presence.

-

- Harvesting pre-existing awareness: Long before legalization, these brands established mindshare via social media or legacy channels. Upon “going legal,” they convert consumers who have been waiting for the “authentic” brand experience.

-

- Capital and supply-chain premium: Backed by stronger funding and larger procurement networks, they can absorb high initial marketing costs and leverage economies of scale to depress hardware costs, enabling faster distribution.

At its core, these brands are not just selling products; they are retaining users. Local brands remain stuck in a transactional disposable logic, and this structural gap is the true battlefield.

The practical threat is simple: a mature brand does not need to “educate” the market from zero. It can arrive with proven packaging, a known name, tested SKUs, retail playbooks, and hardware sourcing already optimized for margin. A local brand that only competes SKU by SKU is fighting a structural opponent with a transactional weapon.

II. Consumer Behavior: The Zero-Loyalty Trap of Disposables

From a behavioral science perspective, the ubiquity of disposables is actively diluting brand loyalty:

-

- Transactional randomness: Disposables are “use-and-toss.” There is no physical bond between the consumer and the brand.

-

- Zero switching costs: Consumers are driven by shelf presence rather than brand affinity. Today they are attracted by cool packaging; tomorrow they switch for a brand that is $2 cheaper.

-

- Structural discontinuity: Every purchase is an isolated decision. Without a retained device, there is no path dependency or habit formation.

If there is no device retention, there is no brand retention. Without a retained device, every vape sale behaves like a new customer acquisition event. The brand must win attention, trust, shelf priority, and price acceptance again and again. This “grab-and-go” habit forces brands to compete for the same floating users repeatedly, driving up customer acquisition costs while failing to build long-term lifetime value.

For cannabis vape brands, this is not only a marketing problem. It is also a margin problem. Every disposable repeats the cost of a battery, heating element, housing, sensor, and final assembly. When hardware is discarded after one cycle, the brand loses both the user relationship and the economic benefit of separating durable hardware from consumable oil.

III. The Structural Gap: Finding the Missing Middle

In the current market, brands are trapped in a strategic dilemma:

-

- Disposables: High conversion efficiency, but zero user retention.

-

- Pod systems: High retention potential, but high entry barriers and difficult conversion.

This implies the market is not lacking a product, but rather a structural layer: a transitional mechanism that captures the initial impulse of a disposable while facilitating the recurring revenue of a pod system. Whoever fills this structural void has the opportunity to build a definitive user moat before the market fully saturates.

| Format |

First-Purchase Barrier |

User Retention |

Cost Structure |

Strategic Risk |

| Disposable |

Low |

Low |

Battery cost repeats in every unit |

Consumers can switch at every purchase |

| Traditional Pod System |

High |

High |

Battery cost separated from refills |

Harder to convert casual disposable buyers |

| Next-gen Pod System |

Designed to feel closer to a disposable entry |

Built around retained battery ownership |

Subsequent pods reduce repeated hardware burden |

Requires clear retail education and compatible pod availability |

The next-gen pod system, at its core, is not a replacement for disposables or pods; it is a fundamental reorganization of the consumption structure. Its core mechanism is to enter the market at a disposable price point while decoupling the hardware into a battery-plus-pod configuration. In essence, the user’s first purchase is not a single-use consumable, but an initial starter kit: battery plus first pod.

The strategic value is not only that the first purchase becomes easier. The strategic value is what happens after the first pod is finished: the consumer already owns the battery, understands the interface, and has a natural reason to buy a compatible refill instead of restarting the purchase journey from zero.

Under this architecture, the consumer’s path is entirely redefined:

-

- Initial touchpoint = pseudo-disposable behavior: The user completes the first purchase with the price expectations and psychological ease of a disposable, lowering the decision barrier.

-

- Physical retention = asset-based lock-in: Once the purchase is made, the battery component is no longer discarded. Instead, it is transformed into a brand asset held in the user’s hand.

-

- Consumption continuity = path convergence: Once the battery becomes a sunk asset, the user’s subsequent repurchases naturally converge into the compatible pod ecosystem.

The result is a psychological pivot: while the consumer appears to be buying a familiar disposable experience, they have actually acquired a hybrid structure of disposable entry plus sustainable repurchase.

Ultimately, it does not change how the user buys; it changes what happens after the purchase. It ensures that once a user finishes their first device, they do not exit the ecosystem. Instead, they are naturally funneled into a pod repurchase path, transforming a fragmented, one-off transaction into a continuous, compounding revenue structure.

For brands and processors, the key metrics should shift from “units sold” alone to refill attach rate, repeat purchase interval, pod repurchase margin, retained battery activation, and retailer reorder velocity.

IV. Strategic Reconstruction: Building a Hardware Moat During the Policy Window

Local brands must realize that current residency requirements and licensing protections are not permanent havens. They are a strategic window for building defensive infrastructure.

1. Securing the Hardware Entry Point

Before mature outside brands can fully flood the market, local brands must establish physical path dependency. The goal is not to force a complex pod system, but to ensure that after the first purchase, the user retains a sustainable device. When the market eventually opens further, the psychological cost of switching, including throwing away a functional device, becomes the local brand’s strongest defense.

In practical terms, this means seeding retained batteries early, supporting them with a focused pod lineup, and ensuring that retail staff can explain the second-purchase logic in one simple sentence: “Keep the battery, replace the pod.”

2. Converting Temporary Regulatory Advantages Into Structural Barriers

Current licensing advantages grant local players initial control over the shelves. Brands must use this to deploy hardware assets that define the user’s behavior path. Once a user begins repurchasing within a specific hardware ecosystem, their subsequent choices naturally converge toward that brand.

The shelf strategy should not be built around one isolated hero SKU. It should be built around a starter kit, compatible refill pods, flavor families, and a merchandising system that makes the next purchase obvious.

3. Optimizing Financial Structure for Future Price Wars

Disposables carry a fixed cost of batteries and sensors in every unit. By transitioning to a system where the battery is a retained asset, the cost of subsequent refills drops significantly. This creates a fatter margin that can be used as marketing ammunition when price wars inevitably begin.

A retained-battery model gives local brands more room to defend margin without relying only on discounting. Instead of absorbing the full device cost in every sale, the brand can shift more value into the oil, pod experience, flavor portfolio, and recurring purchase relationship.

4. Guaranteeing Value Consistency and Professional Credibility

For high-value local extracts, a high-performance pod ensures flavor consistency and reduces the burnt taste often found in cheap disposables. Establishing this reputation for professional-grade delivery early on protects local brands against the variable quality of licensed outside products.

This is especially important for live rosin, high-terpene oil, and premium formulations where poor heating control can damage flavor, increase complaints, and make an expensive extract feel ordinary. Hardware consistency becomes part of brand credibility.

V. Conclusion: Establishing a Regional Defense System

The lesson from New York is clear: if local brands do not build a user retention mechanism during the early stages of legalization, they risk becoming contract fillers for better-known brands with stronger playbooks.

For brands in Ohio and beyond, and for operators preparing for future adult-use markets such as Pennsylvania or Florida if legalization advances, the strategy must evolve. The goal is no longer just to sell more products, but to own the ecosystem. Simply switching to traditional pods may be too heavy; the realistic path is a bridge structure that maintains the conversion speed of a disposable while locking the user into a repeatable system.

The winner will not be the one with the most sales today, but the one with the most users already plugged into its infrastructure tomorrow.

For local cannabis brands, the next move is clear: use the early market window to place retained hardware in consumers’ hands, build a refillable pod path around that hardware, and measure success by repeat purchase rather than one-time sell-through.

-1.webp)

-1.webp)

-2.webp)